December 11, 2025 | House Select Committee on the CCP

Trojan Horse

China's Auto Threat to America

December 11, 2025 | House Select Committee on the CCP

Trojan Horse

China's Auto Threat to America

Hearing Video

December 11, 2025

Download

Full Written Testimony

I. Systemic Incompatibility

China dominates the global automotive sector, producing vast numbers of finished vehicles, components, and parts. China produced more than 30 million vehicles last year — nearly triple U.S. output and far greater than the next-largest producers, Japan and India.[1] While the number of finished vehicles imported directly into the United States from China remains modest, the import of Chinese auto parts, components, and materials has ballooned over the last decade. From 2007 to 2018, China’s share of auto parts imported to the United States nearly doubled in quantity – and its value roughly tripled.[2] Moreover, China’s automotive dominance of foreign markets represents an existential threat to U.S. automakers, stealing American market share abroad and diminishing U.S. auto exports.

Chinese companies’ rapid rise and spread throughout global markets is not a story of competitive success, but of non-market manipulations. China’s automotive lead rests on the back of a state-led system that subsidizes overproduction, manipulates inputs and prices, and treats foreign markets as a pressure release valve for its own structural weaknesses.

China’s economic model prioritizes growth at all costs. U.S. producers ideally create goods to meet demand and, thereby, increase profits — aligning market needs with market incentives. China breaks this fundamental market logic. Production targets are set by politicians to reach national development goals, not purely to address market needs. Hundreds of billions of dollars of subsidies — including buyer credits, municipal tax breaks, subsidized lending, and policies to lower labor costs — go into reinforcing these targets.

Domestic demand in China cannot absorb the volumes that Beijing insists on generating, which is causing deflation in China itself. In a market system, China would curtail its incentives spurring artificial growth and accept losses. While some Chinese authorities have raised the alarm over falling prices and overproduction,[3] the government has been unwilling to make the large structural changes necessary to meaningfully address these issues.

Ultimately, the Chinese Communist Party’s (CCP’s) domestic legitimacy rests on continued economic growth — and the employment and social stability that it provides. As a result, China translates the perverse logic of its political system into a U.S. economic problem, flooding foreign markets, such as ours, with massive amounts of these excess goods — driving down prices and pushing American competitors, who receive few subsidies and protections, out of business. This tactic — and similar non-market practices — leads directly to monopolies and chokepoints across supply chains, as illustrated by the CCP’s coercive restrictions on critical minerals and rare earths, materials that are essential to the automotive industry.

The United States, Mexico, and Canada operate in an open, market-based, rules-based system. China does not. This fundamental mismatch has left North American industry exposed to distorted prices, surging imports, and strategic dependencies that Beijing is increasingly weaponizing. Having built market-dominating monopolies in critical minerals, batteries, magnets, and countless other sectors, China’s authoritarian government is now trying to use that monopoly control to politically coerce the very consumer markets that it depends upon for its own export-driven economic survival. The objective is to lower their trade barriers, tariffs, and other defenses meant to counter China’s predatory practices.

It is not just overproduction that threatens America’s economic strength. China engages in harmful non-market practices that collectively undermine the U.S. industrial base in the automotive sector and beyond.

II. China’s Non-Market Practices

China has built and sustains its influence over the automotive sector by using a range of anti-competitive practices. These measures take advantage of access to markets and competitors who play by the rules — damaging them in the process:

- Subsidies have replaced profit as the key drivers of Chinese economic investment and production. Beginning in the 1990s, China started to approach the automotive sector and related battery sector as “strategically vital industries.”[4] To ensure these industries succeeded, the Chinese government provided huge amounts of financial support. This has included manufacturing grants, low-interest loans, tax exemption and rebates, consumer subsidies, and state and local fleet mandates. These subsidies allow Chines firms to produce new vehicle models in 18 months — three and a half times faster than global competitors[5] — and to largely ignore profitability. While some national-level electric vehicle (EV) subsidies have been phased out, many supply chain and provincial-level incentives remain.Electric vehicles have been a particular Chinese priority. Between 2009 and 2023, China spent $230 billion subsidizing electric vehicles and batteries.[6] Total U.S. EV subsidies during the same period were only a fraction of that amount. As a consequence, only two Chinese EV companies — BYD and Li Auto — are actually profitable, leaving around 30 rivals making losses.[7] These companies survive because of subsidies. The result is massive overproduction, chronic excess capacity, and artificially low prices that undercut market-based producers.

- Monopolies and near-monopolies, especially in critical minerals and battery processes, have choked global supply chains and deterred rival investment. China has consolidated control of key inputs and components, especially for advanced batteries, sensors, and semiconductors. China provides 95 percent of the world’s battery-grade graphite, 85 percent of lithium anodes, 70 percent of cathodes.[8] China controls roughly 95 percent of the global supply of many vital rare earth elements needed for car motors and magnets.[9] Autonomous features in cars, like smart cruise control, generally rely on LiDAR sensors — China is responsible for almost 80 percent of the world’s sales.[10] Many of the parts needed for high-tech “connected” cars are made exclusively in China, raising both supply chain and surveillance concerns. China also produces nearly 60 percent of the world’s primary aluminum supply,[11] needed for engine blocks, wheels, and vehicle frames, and is a central source for chip resistors, capacitors, inductors, and countless other auto components.[12]As seen in recent trade negotiations, China can leverage these monopolies as both a geopolitical weapon against other countries, including the United States,[13] and as a tool of global economic coercion against private sector companies that have little choice but to rely on Chinese inputs.

- Price Manipulation by Chinese entities has distorted global value chains by introducing massive price fluctuations, driving up the price of critical inputs (such as critical minerals) when needed to raise costs on rivals or driving them lower to crush competitors or disincentivize new market entrants.

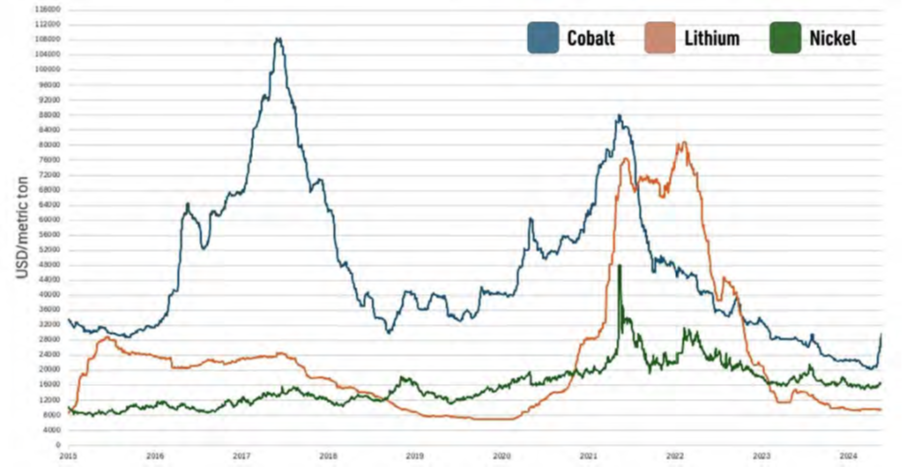

After Chinese state-owned entities successfully lobbied the Indonesian president to impose a ban on exporting raw nickel, Chinese nickel companies — which control 75 percent of Indonesia’s nickel refining — saw a windfall, since refined nickel could still be exported under the ban.[14] Not content to merely benefit from the resulting price spike for refined nickel, Chinese manufacturers went a further step by secretly buying up huge volumes of the refined nickel from the London Metals Exchange (LME), making the largest such withdrawal of nickel in the exchange’s history.[15] Nickel is essential for a number of critical automotive components, from steel to advanced batteries. As a result of the Chinese price manipulations, global competitors essential to the auto sector were severely damaged; Finnish steel producer, Outokumpu, saw its earnings drop by almost 50 percent as a result of high nickel prices.[16]Similarly, Chinese lithium producers reacted to soaring prices in 2021 after the U.S. Inflation Reduction Act by reducing their supply, driving lithium from $7,000 per metric ton in January 2021 to over $75,000 per metric ton by the fourth quarter of 2022. They also prioritized delivery to Chinese companies, so that the harm was felt most by American and other non-Chinese companies. Of course, once global companies responded to high prices by initiating the development of new lithium mining and processing operations to diversify global supply chains and loosen China’s lithium chokehold, China drove in the price through the floor to make non-Chinese projects economically unfeasible.[17] As a result, according to American mining giant Albemarle, as of May 2025, around 40 percent of all global lithium projects are at or below the threshold for profitability at current prices, with one-third of the global capacity having been pulled offline.[18] Chris Ellison, the managing director of western Australian mining company Mineral Resources, suggests the situation is even worse, stating, “No one is making money in this market … let’s be really, really clear on that, there’s no lithium companies making money.”[19]

Price Volatility in Global Cobalt, Lithium, and Nickel Markets (2015-2024)

Graph of the prices for cobalt, lithium, and nickel from 2015 to 2024 in dollars per metric ton. Source: MetalMiner Insights (https://agmetalminer.com).

- Vertical integration has shut out competition and preempted specialization across the automotive sector. Chinese firms face few regulatory constraints on consolidation. Many firms operate across the entire value chain — from mining to refining to software to final assembly. For instance, China’s leading automaker, BYD, not only manufactures cars, maintains its own fleet of ships to transport them, and controls all facets of vehicle distribution, the company also makes a huge number of the components, subcomponents, and raw materials — mining and refining lithium, manufacturing anodes and cathodes, and designing and assembling their own BYD Blade batteries for their globally dominant line of EVs.Even overseas factories are often just assembly shells that leverage massive, vertically integrated China-based operations. In Mexico, Chinese companies commonly import pieces and “kits” from China and perform assembly in Mexico, generating limited benefit for local economies while maintaining market access and legitimacy as “local” production.[20]

- Dumping has driven prices to artificially and anti-competitively low levels. Due in part to subsidies, China can produce almost twice what its domestic market seeks to absorb.[21] For instance, sources suggest that the country is on pace to reach manufacturing capacity for between 2536 million new EVs in 2025[22] despite only about 17 million EVs being sold worldwide in 2024 and anticipated global demand of about20 million EVs in 2025.[23] The remaining surplus is dumped abroad in open, unrestricted markets. China faces more anti-dumping investigations than any other WTO member.[24] A wide range of countries have accused Chinese automakers of selling below cost to drive out competition. In July, the president of the European Commission blamed China for “flooding global markets with cheap, subsidized goods to wipe out competitors.”[25] Even Russia, despite its “no-limits partnership” with Beijing, recently imposed substantial levies on Chinese cars to protect its domestic auto industry from dumping.[26] Mexico, the United Arab Emirates (UAE), Belgium, and the United Kingdom all now absorb more Chinese cars than Russia.[27]

- Labor Abuses, such as forced labor, suppressed wages, and the disregard of basic health, safety, and pollution standards, act as additional non-market subsidies that are not only morally repugnant (which they are), but also give Chinese companies even greater price advantages over market competitors. Extensive reporting shows that forced labor remains widespread in Xinjiang, where Uyghurs and other minorities are compelled to work in state-run programs that feed into auto and battery supply chains. Much of China’s aluminum production is based in Xinjiang, for instance, and is known to rely on exploited Uyghur labor.[28] Aluminum is vital for carmakers, with the auto industry consuming 18 percent of the globally produced metal in 2021.[29]Beyond forced labor, China’s structural labor constraints like the Hukou Residency System. The Hukou System is a household registration regime that sustains a permanent underclass of migrant workers with severely limited economic rights.[30] In practice, the system acts to artificially push down wages for the workers that populate most Chinese factories. Additionally, many provinces lack effective minimum wage enforcement or labor protections, making labor exploitation rampant.[31]Disregard for worker safety and for the impacts of toxic pollutants in China further pushes down costs in ways that American companies cannot — and should not — emulate. For example, China dominates graphite anode production because producers use high-pollution thermal purification, which emits hazardous fine particle pollution and has been linked to serious respiratory illness.[32] In many villages in northeast China, the air literally sparkles from graphite dust.[33] These practices shift health costs onto workers and local communities, while giving Chinese firms a cost advantages that no ethical Western firm can match.

- Intellectual property (IP) theft has supported technology transfer to China. China relies on both legal and illegal technology transfer to build its manufacturing competitiveness. Joint-venture requirements,[34] unfair licensing terms, and state-backed espionage have all historically contributed. Roughly 80 percent of U.S. economic espionage prosecutions involve conduct that benefit the Chinese state.[35] In 2024, a former Tesla employee pled guilty in U.S. federal court to stealing battery-related trade secrets to benefit a Chinese EV supplier,[36] and in 2022, a former engineer pled guilty to stealing autonomous vehicle trade secrets from Apple to benefit a company in China.[37] As technology evolves, China increasingly may be able to steal IP and trade secrets directly from the cars themselves, leveraging connected car technologies, vehicle-generated data, and artificial intelligence (AI).

III. North America’s Shared Vulnerability

While America’s automotive industry benefits from co-production across the whole of North America, market vulnerabilities in Mexico and Canada present major risks to the United States as well. This makes the alignment of trade policies across North America vital.

Chinese automakers are now the top suppliers of completed vehicles to Mexico, surpassing the United States.[38] Though Chinese brands represented less than 1 percent of Mexican new car sales in 2017, they comprised 20 percent of sales by 2024.[39] Chinese automaker BYD entered Mexico’s market in 2023 and, within two years, was on track to match Toyota’s annual sales 22 years after its own entry.[40]

Across the automotive supply chain, China uses its non-market advantages to destroy competition and further bolster market share and monopoly power. In markets around the world, the Chinese Communist Party floods countries with cheap cars and components until local producers are overwhelmed, and ultimately, pushed out of business. This system is unsustainable and unprofitable for China too — but the Chinese government provides its companies with the resources to outlast, and eventually supplant, fair-market competitors.

If America continues to act alone, blocking direct imports of Chinese vehicles or imposing trade barriers on Chinese components, it will not fully insulate the United States from Chinese market pressures. North American automotive production relies on interconnected supply chains. A single part may cross the U.S.-Mexico border more than a half-dozen times before it is integrated into a final product.[41]

That model is powerful, but it’s also vulnerable. Interdependence helps keep costs down via competition and specialization, but it also becomes a weakness when a non-market actor floods one part of the system with below-cost goods. When China dumps artificially cheap products, distorts input prices, or uses Mexico as a workaround for U.S. restrictions, these actions affect the entire supply chain. In addition, competitive pressures have even pushed U.S. automakers to manufacture many of their sedan models in China for import back into North America, taking jobs away from American workers.

Car parts illustrate the scale of the challenge. China accounts for only around 9 percent of all automotive parts imports into the United States, but Chinese parts also enter America through other avenues — circumventing high tariff barriers.[42] For instance, analysts estimate that between 30 and 40 percent of auto parts imported into Mexico from China later enter the United States via either re-export or within assembled vehicles.[43] Between 2013 and 2023, the value of Mexican auto part imports from China grew from $2 billion to almost $5.3 billion, meaning that by 2023, around $2 billion additional Chinese parts presumably ended up in the United States.[44] China is also cornering the after-market auto parts sector in the United States, growing from 2 percent market share in 1995 to more than 40 percent today spread throughout multiple after-market segments.[45] In addition, many Chinese manufacturers of auto parts have also established factories in Mexico. Because parts produced in these factories would generally qualify as “Mexican” under trade rules and be given preferential terms under the United States-Mexico-Canada Agreement (USMCA), the true impact of Chinese auto parts overproduction is largely hidden from view.

Countering Chinese economic pressure requires coordination among North American countries.

IV. Guardrails To Protect Fair Players

As long as overproduction remains essential to the CCP’s political survival, China’s production levels cannot self-correct. Instead, Chinese industry will continue to overproduce until it either kills off all competition or foreign markets are closed off to dumping.

Fortunately, parasitic Chinese economic practices depend on support from a viable host. This makes tariffs and other trade barriers essential to protect American industry, and it forces policymakers to prioritize the alignment of trade restrictions — such as stricter limits regarding rules of origin — with our core trade partners, particularly in North America. As of now, Chinese cars are largely being kept out of the U.S. market (Volvo and Polestar, owned by China’s Geely, are the notable exceptions), but Chinese auto parts are still flowing in and undermining the North American automotive supply chain, both at the manufacturing and aftermarket stages.

To protect our markets and force China to play by the rules, North America must use its leverage to respond in coordination with economic allies:

- Strengthen and Coordinate Trade Barriers. Mexico, Canada, and the United States share concerns about Chinese non-market practices, and the countries’ close collaboration has resulted in shared vulnerabilities. We must coordinate to harmonize higher tariffs on Chinese auto components and vehicles (both EVs and internal combustion vehicles), further tighten rules of origin and labor requirements, and require Chinese firms operating in North America to certify non-compliance with China’s National Intelligence Law before Chinese firms benefit under USMCA. Companies that fail to play by the rules, or engage in monopolistic practices, should face formal “gray listing” in preparation for the possible imposition of economic sanctions. These efforts will meet even greater success if coordination can be expanded to automotive producers outside of North America. Because China’s non-market practices are harmful to any country with an automotive manufacturing or assembling industry, the global threat of a second “China Shock” provides a golden opportunity for the United States to rally a substantial coalition of allies to fight back against Beijing. The United Sates should also encourage its allies and trading partners to pass foreign direct investment laws, patterned after the protocols of the Committee on Foreign Investment in the United States (CFIUS), that review problematic investments and allow for the blocking or unwinding of harmful deals.

- Improve Transparency and Verification. Chinese non-market practices that rely on opacity mask directly illicit activity (like IP theft), product origins, and supply chain connections. Technologies like tagging and tracing tools can be used to verify supply origins and support bolstered rules of origin. The United States should also mandate disclosures from U.S. companies receiving Chinese investment or partnership with Chinese-linked entities. China should not get to benefit from U.S. markets while undercutting them.

- Build More Resilient Critical Mineral Supply Chains. The United States and its allies should support new investments in the minerals, resources, and technologies central to the future of the automotive sector. This can protect U.S supply chains from Chinese monopolization and manipulation.In the United States, the U.S. government should promote private investment in mining and processing through matching funds with equity stakes, low lease rates for public land, public sector-backed risk insurance, and pricing mechanisms independent of Chinese influence. Revisions to Bureau of Land Management and U.S. Forest Service land use regulations, leases, and permits could allow for private mineral extraction on public lands. The executive branch should consolidate permitting and environmental regulations into a single process that simultaneously addresses federal, state, and local concerns, leveraging the FAST-41 process that Congress created in 2015. Congress should establish a pilot program that provides new litigation rules under the Administrative Procedure Act or a new statute to (a) limit the initiation of lawsuits challenging new projects to between 90- and 180-days post permit filing, (b) expedite such cases via a “rocket docket,” (c) and process lawsuits in a statutorily approved uniform federal venue.In allied countries, the U.S. Development Finance Corporation (DFC), a key player in incentivizing overseas U.S. investments, needs to be reauthorized with the flexibility to work wherever our supply chains demand — even if that is in upper-middle or high-income countries. For instance, DFC should consider partnership with Mexico to process its abundant clay-based lithium reserves and to assist with establishing North American processing for a wide range of critical minerals. DFC financing should be conditioned on the unwinding of Chinese investments, supply chains, and debt entanglement.The United States and its allies should also align to set temporary price floors on selected minerals (notably, lithium, nickel, cobalt, and graphite) acquired from non-Chinese sources. The floors would apply as needed to government procurement, offtake agreements, defense contractors, and government-funded energy projects to incentivize further capital investments. As a first step, the Defense Logistics Agency (DLA) should revise its stockpiling procurement model. Instead of relying solely on lowest price bids, DLA could adopt a “minimum sustainable production cost” standard for critical minerals from allied nations over five to 10 years. Comparable approaches exist in U.S. energy and agriculture markets (e.g., Department of Agriculture-guaranteed pricing for biomass and Department of Energy (DOE) solar power purchasing agreement frameworks).

- Use Innovation to Break Chinese Monopolies. The federal government should offer targeted, time-limited subsidies for promising new technologies that reduce dependence on Chinese monopolies. Congress should amend the tax code to provide full cost recovery for research and development (R&D) and equipment investment. For instance, Niron Magnetics, a Minnesota-based company that was spun out of federally funded research, is making high-powered magnets without Chinese controlled rare earth elements and creating new manufacturing jobs in the United States. Long-term research investments should be scored, in part, on their ability to break Chinese monopolies. In addition, Congress should develop mechanisms under the Defense Production Act for the U.S. government to acquire promising technology from bankrupt companies, such as providing the DOE with a right of first refusal to purchase subsidized intellectual property.

- Build An Economic Warfare Doctrine. Chinese non-market practices are a problem much larger than the automotive sector. We would never deploy U.S. forces abroad without a joint doctrine, a common operational picture, or surge capacity. Yet that is how we conduct economic warfare today — scattershot across multiple sectors. We need a government structure built for purpose — one capable of collecting and analyzing comprehensive data on trade flows, sanctions evasion networks, supply chain dependencies, and export control risks — and acting on them decisively. The National Security Council — or a new Economic Security Coordination Office within the executive branch — should set a strategic framework for economic statecraft that clarifies why, how, and to what end we must act. This will require a complete review of existing economic security functions across our government and a forward-looking approach to unify these tools under a coherent set of foundational operating principles.

V. Conclusion

China’s non-market practices in the automotive sector are not a temporary challenge; they reflect a deliberate strategy to dominate a foundational global industry. The United States, Mexico, and Canada cannot treat conflict with China’s automotive sector like a routine trade dispute. This structural threat distorts markets, weakens supply chains, and increases strategic vulnerability.

America’s automotive industry is one of our greatest economic assets and a part of our heritage. Protecting it requires policies that match the scale of the challenge.

Thank you for the opportunity to testify.

[1] “World Motor Vehicle Production by Country/Region and Type,” International Organization of Motor Vehicle Manufacturers, accessed December 8, 2025. (https://oica.net/wp-content/uploads/2025/10/By-country-region-2024.pdf)

[2] David Coffin, “China’s Growing Role in U.S. Automotive Supply Chains,” U.S. International Trade Commission, Office of Industries, August 2019, page 1. (https://www.usitc.gov/publications/332/working_papers/id-19-060_chinese_auto_parts_final_080519-compliant_0.pdf)

[3] “The brutal fight to dominate Chinese carmaking,” The Economist (UK), September 15, 2025. (https://www.economist.com/business/2025/09/15/the-brutal-fight-to-dominate-chinese-carmaking)

[4] Adam Bernard, “The Rise of Chinese Automakers,” Car and Driver, October 25, 2025. (https://www.caranddriver.com/features/a69123018/the-rise-of-chinese-automakers); Yisong Chen, Xiaofang Dai, Pei Fu, Geng Luo, and Peilong Shi, “A review of China’s automotive industry policy: Recent developments and future trends,” Journal of Traffic and Transportation Engineering, October 2024, pages 867-895. (https://www.sciencedirect.com/science/article/pii/S2095756424000989)

[5] “China’s Auto Industry Leaves Competitors in the Dust Due to Its Agility,” Institute for Energy Research, September 2, 2025. (https://www.instituteforenergyresearch.org/international-issues/chinas-auto-industry-leaves-competitors-in-the-dust-due-to-its-agility)

[6] Scott Kennedy, “The Chinese EV Dilemma: Subsidized Yet Striking,” Center for Strategic and International Studies, June 20, 2024. (https://www.csis.org/blogs/trustee-china-hand/chinese-ev-dilemma-subsidized-yet-striking)

[7] Daniel Ren, “China’s EV Makers Are Selling More Vehicles at Bigger Losses, as Price War Takes Its Toll,” South China Morning Post (China), August 23, 2024. (https://www.scmp.com/business/china-business/article/3275699/chinese-ev-makers-losses-mount-rising-sales-fail-offset-steep-discounts)

[8] Elaine K. Dezenski and Josh Birenbaum, “Unplugging Beijing: A Playbook to Reclaim America’s Advanced Battery Supply Chain,” Foundation for Defense of Democracies, July 21, 2025. (https://www.fdd.org/analysis/2025/07/21/unplugging-beijing)

[9] Divya Rajagopal, “Western miners seek premium pricing for rare earth metals to break China grip,” Reuters, November 8, 2023. (https://www.reuters.com/markets/commodities/western-miners-seek-premium-pricing-rare-earth-metals-break-china-grip-2023-11-08)

[10] “Policy Alert: Urgent U.S. Response Needed to Counter China’s Strategic Use of LiDAR Technology,” FDD Action, September 23, 2025. (https://www.fddaction.org/policy-alerts/2025/09/23/policy-alert-urgent-u-s-response-needed-to-counter-chinas-strategic-use-of-lidar-technology)

[11] “The Development of Aluminum Industry and Technology in China,” International Aluminium Institute, February 2024, page 1. (https://international-aluminium.org/wp-content/uploads/2024/02/The-Development-of-Aluminum-Industry-and-Technology-in-China-1.pdf)

[12] Michael Mariani, “Just How Dependent Is the Automotive Industry on Electronic Components Manufactured in China?” Z2Data, April 23, 2025. (https://www.z2data.com/insights/how-dependent-automotive-industry-on-electronic-components-manufactured-china)

[13] Tae-Yoon Kim, Shobhan Dhir, Amrita Dasgupta, and Alessio Scanziani, “With New Export Controls on Critical Minerals, Supply Concentration Risks Become Reality,” International Energy Agency, October 23, 2025. (https://www.iea.org/commentaries/with-new-export-controls-on-critical-minerals-supply-concentration-risks-become-reality)

[14] Henry Sanderson, Volt Rush: The Winners and Losers in the Race to Go Green (London: Oneworld Publications, 2022), pages 159-160; “Chinese firms control around 75% of Indonesian nickel capacity, report finds,” Reuters, February 5, 2025. (https://www.reuters.com/markets/commodities/chinese-firms-control-around-75-indonesian-nickel-capacity-report-finds-2025-02-05)

[15] Alfred Cang and Mark Burton, “China’s Tsingshan Helped Drive Record Drop in Nickel Inventories,” Bloomberg, October 8, 2019. (https://www.bloomberg.com/news/articles/2019-10-08/china-s-tsingshan-helped-drive-record-drop-in-nickel-inventories)

[16] Henry Sanderson, Volt Rush: The Winners and Losers in the Race to Go Green (London: Oneworld Publications, 2022), page 159.

[17] Elaine K. Dezenski and Josh Birenbaum, “Unplugging Beijing: A Playbook to Reclaim America’s Advanced Battery Supply Chain,” Foundation for Defense of Democracies, July 21, 2025, page 37. (https://www.fdd.org/analysis/2025/07/21/unplugging-beijing)

[18] Meredith Bandy, Kent Masters, Neal Sheorey, Netha Johnson, and Eric Norris, “Albemarle Corporation (NYSE:ALB) Q1 2025 Earnings Call Transcript,” Insider Monkey, May 2, 2025. (https://www.insidermonkey.com/blog/albemarle-corporation-nysealb-q1-2025-earnings-calltranscript-1523250)

[19] Adrian Rauso, “Mineral Resources and Pilbara Minerals Among Lithium Stocks Skyrocketing as China Closes Down Huge Mine,” The Nightly (Australia), September 10, 2024. (https://thenightly.com.au/business/mining/mineral-resources-and-pilbara-minerals-among-lithium-stocks-skyrocketing-as-china-closes-down-huge-mine–c-16016679)

[20] Margaret Myers and Yifang Wang, “China’s Pressure in Mexico’s Auto Sector: What’s at Stake for Mexico,” Inter-American Dialogue, August 2025. (https://thedialogue.org/wp-content/uploads/2025/08/Whats-at-Stake-for-Mexico-PubVer.pdf)

[21] Agnes Chang and Keith Bradsher, “How China Became the World’s Largest Car Exporter,” The New York Times, November 29, 2024. (https://www.nytimes.com/interactive/2024/11/29/business/china-cars-sales-exports.html)

[22] “新能源汽车内卷真相 (The Truth Behind the Involution of New Energy Vehicles),” The Paper (China), June 8, 2024. (https://www.thepaper.cn/newsDetail_forward_27662060); Brad W. Setser, “Will China Take Over the Global Auto Industry?” Council on Foreign Relations, December 8, 2024. (https://www.cfr.org/blog/will-china-take-over-global-auto-industry)

[23] International Energy Agency, “Global EV Outlook 2025,” May 14, 2025. (https://iea.blob.core.windows.net/assets/0aa4762f-c1cb-4495-987a-25945d6de5e8/GlobalEVOutlook2025.pdf)

[24] Lu Cheng, Zhifu Mi, D’Maris Coffman, Jing Meng, and Dongfeng Chang, “Destruction and Deflection: Evidence from American Antidumping Actions against China,” Structural Change and Economic Dynamics, June 2021, pages 203-213. (https://www.sciencedirect.com/science/article/abs/pii/S0954349X2100031X)

[25] David Pierson and Berry Wang, “China Stood Up to Trump, and It’s Not Giving Europe an Inch, Either,” The New York Times, July 21, 2025. (http://nytimes.com/2025/07/21/world/asia/china-europe-trade-war.html)

[26] Gregor Sebastian, “Collision Course: The Future of Chinese Carmakers in Russia,” Rhodium Group, December 12, 2024. (https://rhg.com/research/collision-course-the-future-of-chinese-carmakers-in-russia); Nick Carey, “China floods the world with gasoline cars it can’t sell at home,” Reuters, December 2, 2025. (https://www.reuters.com/investigations/china-floods-world-with-gasoline-cars-it-cant-sell-home-2025-12-02)

[27] “China Will Make Almost a Third of the World’s Cars by 2030,” Bloomberg News, July 17, 2025. (https://www.bloomberg.com/graphics/2025-china-ev-byd-global-price-cuts)

[28] Human Rights Watch, “Asleep at the Wheel: Car Companies’ Complicity in Forced Labor in China,” February 1, 2024. (https://www.hrw.org/report/2024/02/01/asleep-wheel/car-companies-complicity-forced-labor-china)

[29] Ibid.

[30] Qingyi Huang, “From Socialism to Stratification: The Unfinished Reform of China’s Hukou System,” Synergy: The Journal of Contemporary Asian Studies, April 9, 2025. (https://utsynergyjournal.org/2025/04/09/from-socialism-to-stratification-the-unfinished-reform-of-chinas-hukou-system)

[31] Yanan Li, Ravi Kanbur, and Carl Lin, “Minimum Wage Competition between Local Governments in China,” IZA Institute of Labor Economics, updated May 2025. (https://papers.ssrn.com/sol3/papers.cfm?abstract_id=3273733)

[32] Peter Whoriskey, “In Your Phone, In Their Air,” The Washington Post, October 2, 2016. (https://www.washingtonpost.com/graphics/business/batteries/graphite-mining-pollution-in-china)

[33] Ibid.

[34]Adam Bernard, “The Rise of Chinese Automakers,” Car and Driver, October 25, 2025. (https://www.caranddriver.com/features/a69123018/the-rise-of-chinese-automakers)

[35] U.S. Department of Justice, National Security Division, “Information About the Department of Justice’s China Initiative and a Compilation of China-Related Prosecutions Since 2018,” November 19, 2021. (https://www.justice.gov/archives/nsd/information-about-department-justice-s-china-initiative-and-compilation-china-related)

[36] U.S. Department of Justice, Press Release, “Resident of China Sentenced to 24 Months in Prison for Conspiring to Send Trade Secrets Belonging to U.S. Company,” December 16, 2024. (https://www.justice.gov/usao-edny/pr/resident-china-sentenced-24-months-prison-conspiring-send-trade-secrets-belonging)

[37]Stephen Nellis, “Former Apple car engineer pleads guilty to trade secret theft,” Reuters, August 23, 2022. (https://www.reuters.com/legal/former-apple-car-engineer-pleads-guilty-trade-secret-theft-2022-08-23); U.S. Department of Justice, Press Release, “Former Apple Employee Indicted for Theft of Trade Secrets,” July 16, 2018. (https://www.justice.gov/usao-ndca/pr/former-apple-employee-indicted-theft-trade-secrets)

[38] Teresa De Alba, “China Becomes Mexico’s Top Car Supplier in Early 2025,” Mexico Business News (Mexico), July 8, 2025. (https://mexicobusiness.news/automotive/news/china-becomes-mexicos-top-car-supplier-early-2025)

[39] Ibid.

[40] Michael Dunne, “Analysis: Chinese cars pour in to Mexico, rattling the USMCA,” Mexico News Daily (Mexico), November 20, 2024. (https://mexiconewsdaily.com/business/analysis-chinese-cars-mexico-usmca)

[41] Norman De Bono, “Trump tariffs: How one car piece crosses Canada, U.S., Mexico borders 7 times,” London Free Press (Canada), March 6, 2025. (https://lfpress.com/news/local-news/trump-tariffs-car-part-crosses-canada-us-mexico-borders-7-times); Thanos Pappas, “One Piston Crosses Six Borders Before It Powers Your American-Made Truck,” Carscoops, April 3, 2025. (https://www.carscoops.com/2025/04/us-made-cars-and-trucks-are-not-really-safe-from-trumps-tariffs)

[42] “US Imports of Automotive Parts by Country 2011-2024,” Automotive Aftermarket, April 22, 2025. (https://automotiveaftermarket.org/automotive-parts-imports-country)

[43] Claire Yuan, Stephen Chan, Charles Chang, Danny Huang, and Crystal Ling, “Mexican Tariffs: A Speedbump To Chinese Auto Firms’ Overseas Expansion,” S&P Global, September 17, 2025. (https://www.spglobal.com/ratings/en/regulatory/article/mexican-tariffs-a-speedbump-to-chinese-auto-firms-overseas-expansion-s101645512)

[44] David Coffin, Sharon Ford, and Edward Petronzio, “Chinese Automotive and Electronics Trade and Investment in Mexico,” U.S. International Trade Commission, Office of Industry and Competitiveness Analysis, November 2024, page 12. (https://www.usitc.gov/publications/332/working_papers/chinese_aei_mexico.pdf)

[45] “The Growing Threat of Chinese Aftermarket Auto Parts in the U.S.,” Emerging Strategy, March 6, 2025. (https://www.emerging-strategy.com/the-growing-threat-of-chinese-aftermarket-auto-parts-in-the-u-s)